.jpg)

Pay By Touch's ATM Direct Looks to Add Another Network, More Online Retailers

ATM Direct, which this week announced agreements with an electronic funds transfer network and an Internet merchant to process PIN-secured debit card payments on the Web, has signed another online retailer, which will go live on its system in August.

This second, unnamed merchant, which does $250 million annually in Web sales, could be followed later in the summer by a third, Ziegler says, with which ATM Direct is now in talks. In addition, the company, a unit of biometric-payments processor Pay By Touch Inc., San Francisco, also plans to bring live a link to a second EFT network within 90 days, Ziegler says.

For 2007, Ziegler says, look for ATM Direct to process PIN debit payments on handsets as it rolls out a mobile version of its software.

Also on tap for next year, he adds, is a recurring-payment capability for utilities and other biller categories that may now accept so-called PIN-less debit transactions.

When launched, this product will allow these billers for the first time to accept recurring debit card payments, since EFT network operating rules currently do not permit recurring payments using PIN-less debit.

The flurry of developments caps months of behind-the-scenes work by the company, whose software allows consumers to enter debit card PINs securely on a computer screen, to bring its product to market following its acquisition last year by Pay By Touch (Digital Transactions News, Dec. 16, 2005).

Those efforts bore fruit this week with the announcements that the Bellevue, Wash.-based ACCEL/Exchange network has agreed to switch transactions processed by ATM Direct (Digital Transactions News, June 5) and that The J. Paul Co., a Dallas promotional-goods merchant, in July will begin accepting PIN debit payments on its Web site through ATM Direct.

Transactions will build over time, Ziegler says, as more and more of ACCEL/Exchange’s 3,500 banks bring their cards live on the system. “It’s a managed rollout,” he says. “Some issuers will be able to transact immediately, and we’ll add others over time. We want everyone on the network to have a real good experience.”

By year’s end, he projects, some 60% of ACCEL/Exchange’s 80 million cards will be enabled for ATM Direct. Transaction growth should accelerate, too, with the addition of the second EFT Network, which Ziegler refuses to name, as well as the large retailer.

ATM Direct’s selling proposition to smaller merchants is lower transactions costs, coupled with the fraud-management and guaranteed-funds features traditionally offered by PIN debit cards.

For larger retailers, says Ziegler, his product’s appeal lies in a 5% to 6% incremental sales increase the company’s research shows online merchants can gain by enabling customers to pay with PIN debit.

Though he won’t give specific pricing, he says ATM Direct’s fees to merchants should result in acceptance costs that are on average about half what e-commerce sellers now pay in card-not-present rates. Larger merchants will enjoy a bigger break, he says. Pricing, he says, will follow “multiple models,” sometimes including both percentage and fixed-fee components, sometimes not.

ATM Direct’s system works by downloading digitally unique code to the consumer's desktop, setting up a process of multifactor authentication in which the company can authenticate the consumer by recognizing the code and by means of technology such as geo-location. The company also sweeps the consumer’s PC for keyloggers and other trojans.

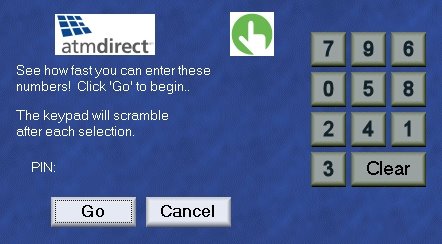

When the consumer is ready to buy and ATM Direct is satisfied the PC is secure, the system presents on the screen a keypad for PIN entry.

The pad is called a floating PIN pad because a different numerical configuration is presented each time. This process disables the computer keyboard, allowing entry only by mouse click. Once PIN entry is complete, ATM Direct returns a signed token to the merchant, asking if the merchant wants to go forward with authorization. If so, it creates a transaction message, including a PIN block with PINs encrypted at two-key triple DES, to go to the relevant EFT network for authorization and settlement at the issuing bank. In this sense, it operates as if it were another processor hooked into the EFT network’s switch.

The pad is called a floating PIN pad because a different numerical configuration is presented each time. This process disables the computer keyboard, allowing entry only by mouse click. Once PIN entry is complete, ATM Direct returns a signed token to the merchant, asking if the merchant wants to go forward with authorization. If so, it creates a transaction message, including a PIN block with PINs encrypted at two-key triple DES, to go to the relevant EFT network for authorization and settlement at the issuing bank. In this sense, it operates as if it were another processor hooked into the EFT network’s switch.