As previously mentioned, shoppers at Chicago-area Jewel-Osco stores can now pay for their groceries by swiping a finger over a scanner. No need to pull out your checkbook or debit card or even your Jewel Preferred card.

Jewel-Osco is the largest grocery store chain to adopt the biometric technology, which Jewel-Osco President Larry Wahlstrom touted as a safer, faster way for customers to pay their bills.

With the Pay By Touch launch at 200+ Jewel-Osco stores this week, Chicago becomes the largest grocery marketplace nationwide to use the finger-scan technology. Cub Foods' 35 local stores, including one in Naperville, started using the technology in November.

People who are already registered with the Pay By Touch system can use it wherever it is offered.

In 10 months, Pay By Touch has grown from having its finger-scanning system in 50 stores to being in 2,100 stores.

Stand-alone Osco drugstores do not have the technology. Retailers tout the technology for helping shoppers dash through the checkout, no longer fumbling with ID cards and key fobs, and leaving their purses and wallets at home. But retailers benefit and save money, too. Grocery stores that use the technology no longer pay banks and other intermediaries to process credit card and paper check payments.

With the finger-scan technology, Pay By Touch Solutions charges the retailer slightly more than 10 cents per transaction and processes the payment automatically through a bank-to-bank clearinghouse. The faster system saves the grocery store money and speeds the payment.

John Morris, president and chief operating officer of Pay By Touch Solutions, the San Francisco company that provides the technology, said, "We're capturing and comparing a set of unique descriptors about a person's biometric without storing the image. "The set of descriptors could not be used to regenerate a fingerprint," said Morris, who lives in Hinsdale and commutes to work in California.

.jpg)

Friday, March 31, 2006

Thursday, March 30, 2006

Bread Box' 19 Stores Implement PBT

KnoxNews: Business (subscription)

Bread Box stores step into future to offer biometric pay system

By CYNTHIA YELDELL, yeldellc@knews.com March 30, 2006

It's been perceived as clever, cool, a fad, an invasion of privacy or something out of a science fiction novel, but many retailers agree that biometric payments are the wave of the future.

Bread Box, a Knoxville area convenience store chain, says it's the first company in Tennessee to give customers the option to pay for items with only the touch of a finger.

Bread Box, a Knoxville area convenience store chain, says it's the first company in Tennessee to give customers the option to pay for items with only the touch of a finger.

The company's new BioPay system eliminates the need for checks, cash and other traditional payment methods by taking a finger scan that identifies customers by reading points of their fingerprints. Payments are automatically deducted from the shopper's checking account.

While privacy advocates are concerned about government tracking, Bread Box President Chuck Baine said the system is safe and convenient. Baine said the system virtually eliminates identity theft while also reducing his payment processing costs, allowing him to pass those savings along to customers.

"You can image a period where you wouldn't need a wallet," Baine said. "It's really simple, and it makes sense." BioPay is a biometric services provider that's owned by Pay By Touch, a San Francisco-based company that provides biometric authentication, loyalty, membership and payment services. Pay By Touch paid a reported $82 million in cash and stock for Virginia-based BioPay in December.

BioPay says it offers customers a speedy check out and enhances security since "your finger is unique to you." Baines sees it as a "way to differentiate ourselves and do new things that are fun to customers." Customers have their finger scanned inside the stores. BioPay doesn't have systems that allow finger scans at the pump, Baine said, but he expects that technology to be available later this year and he will add it to his locations.

Baine expects competitors to add similar biometric systems once they become available at the pump, but he is trying to stay a step ahead. He said the system could potentially save him thousands of dollars in credit card processing costs.

Since gas prices have risen, Baine said, more customers have switched to credit-card payments, which can cost him 7 or 8 cents per gallon. Baine paid $700,000 in credit-card processing fees last year. Bread Box has 19 locations in the Knoxville area that generate $70 million in sales annually.

"In the beginning it's not going to save a lot of money," Baine said. "I hope to develop a culture to get people using BioPay and switch credit-card customers over." As an incentive, Baine is taking a nickel off the price of each gallon of gasoline purchased in April for customers who sign up.

Predictably, customers have mixed feelings about the system.

Charles Fulford said he would have to weigh the pros and cons. "It's clever and interesting," Fulford said, adding that he would want to know who has access to the information. "I would have to know it's going to be taken seriously and not a passing fad or gimmick." Alison Kirk, a 21-year-old Bread Box customer, would be willing to experiment. "It's kind of cool, but it makes me a little nervous," she said.

BioPay maintains that the system is secure because the consumer leaves behind no personal information. The company also says it prevents identity theft because only the person matching the finger scan can use the account.

Biometric technology has been around for years, said Hussain Shah, a marketing assistant for the company. It has been widely used in the security industry. Retailers first used the technology for identification of customers who needed to cash checks. Several area Bi-Lo grocery stores had used BioPay for check cashing but those locations were sold to Food City, which does not use it.

Shah said BioPay was first used as a payment option in 2003 and more than 2,000 retailers, grocery stores and restaurants now use it.

The company has more than 2 million customers. Fortune Magazine reported recently that Wal-Mart and Costco are believed to be looking into biometric payment systems.

Bread Box stores step into future to offer biometric pay system

By CYNTHIA YELDELL, yeldellc@knews.com March 30, 2006

It's been perceived as clever, cool, a fad, an invasion of privacy or something out of a science fiction novel, but many retailers agree that biometric payments are the wave of the future.

Bread Box, a Knoxville area convenience store chain, says it's the first company in Tennessee to give customers the option to pay for items with only the touch of a finger.

Bread Box, a Knoxville area convenience store chain, says it's the first company in Tennessee to give customers the option to pay for items with only the touch of a finger.The company's new BioPay system eliminates the need for checks, cash and other traditional payment methods by taking a finger scan that identifies customers by reading points of their fingerprints. Payments are automatically deducted from the shopper's checking account.

While privacy advocates are concerned about government tracking, Bread Box President Chuck Baine said the system is safe and convenient. Baine said the system virtually eliminates identity theft while also reducing his payment processing costs, allowing him to pass those savings along to customers.

"You can image a period where you wouldn't need a wallet," Baine said. "It's really simple, and it makes sense." BioPay is a biometric services provider that's owned by Pay By Touch, a San Francisco-based company that provides biometric authentication, loyalty, membership and payment services. Pay By Touch paid a reported $82 million in cash and stock for Virginia-based BioPay in December.

BioPay says it offers customers a speedy check out and enhances security since "your finger is unique to you." Baines sees it as a "way to differentiate ourselves and do new things that are fun to customers." Customers have their finger scanned inside the stores. BioPay doesn't have systems that allow finger scans at the pump, Baine said, but he expects that technology to be available later this year and he will add it to his locations.

Baine expects competitors to add similar biometric systems once they become available at the pump, but he is trying to stay a step ahead. He said the system could potentially save him thousands of dollars in credit card processing costs.

Since gas prices have risen, Baine said, more customers have switched to credit-card payments, which can cost him 7 or 8 cents per gallon. Baine paid $700,000 in credit-card processing fees last year. Bread Box has 19 locations in the Knoxville area that generate $70 million in sales annually.

"In the beginning it's not going to save a lot of money," Baine said. "I hope to develop a culture to get people using BioPay and switch credit-card customers over." As an incentive, Baine is taking a nickel off the price of each gallon of gasoline purchased in April for customers who sign up.

Predictably, customers have mixed feelings about the system.

Charles Fulford said he would have to weigh the pros and cons. "It's clever and interesting," Fulford said, adding that he would want to know who has access to the information. "I would have to know it's going to be taken seriously and not a passing fad or gimmick." Alison Kirk, a 21-year-old Bread Box customer, would be willing to experiment. "It's kind of cool, but it makes me a little nervous," she said.

BioPay maintains that the system is secure because the consumer leaves behind no personal information. The company also says it prevents identity theft because only the person matching the finger scan can use the account.

Biometric technology has been around for years, said Hussain Shah, a marketing assistant for the company. It has been widely used in the security industry. Retailers first used the technology for identification of customers who needed to cash checks. Several area Bi-Lo grocery stores had used BioPay for check cashing but those locations were sold to Food City, which does not use it.

Shah said BioPay was first used as a payment option in 2003 and more than 2,000 retailers, grocery stores and restaurants now use it.

The company has more than 2 million customers. Fortune Magazine reported recently that Wal-Mart and Costco are believed to be looking into biometric payment systems.

Tuesday, March 28, 2006

Biometrics: Payments at Your Fingertips

Fingerscans will replace credit cards

Fingerscans will replace credit cardsThat is, if companies like Pay By Touch have anything to say about it.

Pay By Touch, a closely held San Francisco outfit, specializes in biometrics, or the technology of identifying people by unique biologic traits -- not just fingerprints, but also irises, palms, and voices. And increasingly, those traits are being used in place of keys, credit cards, and even computer passwords.

Founded in 2002, Pay By Touch has signed up more than 2 million people willing to have their fingerprints used as a surrogate for checks and credit cards at more than 2,000 stores, including several large grocery chains. When making a purchase, a customer presses his pointer finger to a pad and then keys in an identifying number as an added security measure before his purchase is deducted from a checking account or added to a credit-card bill.

On Mar. 21, Pay By Touch said its device would be installed in all of Albertson's (ABS) Jewel-Osco stores, a chain of more than 200 outlets that combine supermarkets and pharmacies.

KEEP OUT. It's not just stores that are using biometrics. Elementary schools have installed iris scanners to keep out intruders. Companies increasingly use fingerprint scanners to authenticate computer users. And fingerprint readers have also been installed on locks for house and office doors.

Many consider Pay By Touch to be among the companies most effectively harnessing the rising demand for biometrics. Pay By Touch charges a set fee for each positively identified fingerprint that can run in the neighborhood of 15 cents for a big retailer, according to Pay By Touch President and Chief Operating Officer John Morris.

What's in it for the store? Using fingerprint scanners can accelerate purchase times by minimizing the checkout lane "fumble factor." Because a customer's Pay By Touch account can be linked to several payment devices, retailers can also save money by encouraging people to use accounts that incur lower fees, such as a checking account accessed by debit card. One east coast retailer projects savings of $3.2 million dollars on Interchange Fees thanks to their implementaion of PBT.

A recent report by Bernstein Research noted that systems like Pay By Touch could increase pressure on credit-card companies to reduce their charges to retailers so they don't lose market share.

BARGAIN ALERT. Supermarket owners overall say they're pleased with Pay By Touch results. "We'd like to encourage anybody who has a checking account to enroll in Pay By Touch," says Trisha Belisle, manager of retail technology at Cub Foods, a Midwest supermarket chain owned by Supervalu (SVU). She declined to comment on whether it saves the stores money, however.

Pay By Touch is also experimenting with using the system to customize bargains to individual shoppers based on their past purchases, a trick the Sunday newspaper circular could never manage. Advocates say biometrics is a better safeguard against identity theft than current methods. It's easier, after all, to obtain a credit-card number than a fingerprint or voice pattern.

Pay By Touch hopes to ride the wave as far as it can. In January it acquired rival BioPay for $82 million and recently closed on $60 million in capital from hedge funds and private investors. This came about three months after the company announced raising an additional $130 million. Morris declined to discuss sales or any plans the company might have to go public. But Pay By Touch expects to double sales this year from 2005, in part due to acquisitions.

ONLINE AMBITIONS. Morris says the company hopes to expand its services to include health insurance information. It also has an initiative that would let customers use fingerprints to make online purchases using the sensors available on some laptops. It plans to announce a participating online store later this year (see BW Online, "Promising Pitches at Demo 2006").

Friday, March 24, 2006

Pay by Touch Payment Solutions

www.paybytouchpaymentsolutions.com

Key Facts & Figures

Key Facts & Figures

Offices in Atlanta, Georgia, Tucson, Arizona, and New Castle, Delaware

In operation for more than 15 years

Processes transactions for over 130,000 small to mid-sized businesses

Processes more than $18 billion in Visa, MasterCard, American Express, Discover, on-line debit and EBT transactions annually

Experienced Management Team

Average of 15 years experience in financial services and payment processing

Experience at top financial services firms, including Chase Manhattan, First Data, MasterCard

Operational expertise in latest fraud/account opening technologies

Educational backgrounds in finance, business/risk management, and banking

State-of-the-Art Technology

Unique, proprietary authorization network

Direct dial, web-based, or dedicated network connectivity for high-speed, secure processing

VISA Cardholder Information Security Program (CISP) Compliant

Proven history of stability and reliability

The Pay By Touch Payment Solutions Difference

Single source, end-to-end payment processing provider

Customizable solution sets designed for today's merchant

Management reporting and unique value-added services

Cost-effective pricing

Exceptional customer service and support

Key Facts & Figures

Key Facts & FiguresOffices in Atlanta, Georgia, Tucson, Arizona, and New Castle, Delaware

In operation for more than 15 years

Processes transactions for over 130,000 small to mid-sized businesses

Processes more than $18 billion in Visa, MasterCard, American Express, Discover, on-line debit and EBT transactions annually

Experienced Management Team

Average of 15 years experience in financial services and payment processing

Experience at top financial services firms, including Chase Manhattan, First Data, MasterCard

Operational expertise in latest fraud/account opening technologies

Educational backgrounds in finance, business/risk management, and banking

State-of-the-Art Technology

Unique, proprietary authorization network

Direct dial, web-based, or dedicated network connectivity for high-speed, secure processing

VISA Cardholder Information Security Program (CISP) Compliant

Proven history of stability and reliability

The Pay By Touch Payment Solutions Difference

Single source, end-to-end payment processing provider

Customizable solution sets designed for today's merchant

Management reporting and unique value-added services

Cost-effective pricing

Exceptional customer service and support

Wednesday, March 22, 2006

Chicago Advertising Campaign to Launch

Pay By Touch Looks for ‘Network Effect’ from Chicago Concentration

TV and Radio Advertising Campaign Slated to Begin April 5th

Electronic point-of-sale transactions secured by biometric scans may get a boost now that Pay By Touch Inc. has switched on processing service in 204 Jewel-Osco stores in the Chicago area.

Electronic point-of-sale transactions secured by biometric scans may get a boost now that Pay By Touch Inc. has switched on processing service in 204 Jewel-Osco stores in the Chicago area.

The San Francisco company’s latest implementation represents its most concentrated installation in a metropolitan area so far. With many Jewel customers often shopping at more than one store in the chain, Pay By Touch hopes to get a lift in transaction volume. “This is the first time we’re going to see the network effect in action,” says Shannon Riordan, director of marketing for the company, whose technology allows merchants to authenticate customers via fingerprint scans. “We think that will be a driver of usage [in the Chicago area].”

In addition to the Jewel stores, Pay By Touch has been processing transactions for 35 Cub Foods stores in the Chicago metropolitan area for the past four months. These stores were until recently owned by Supervalu Inc.

TV and Radio Advertising Campaign

The market concentration also allows Pay By Touch to conduct marketwide consumer advertising for the service for the first time. Riordan says beginning in early April, advertising for the service will appear on radio and TV as well as in newspaper circulars placed by Jewel. “The time [for biometric payments] is now,” says Riordan. “It’s not a thing of the future any more.”

The Jewel installation follows a test by parent company Albertsons Inc. in four Portland, Ore., stores, which started in January 2005. Riordan, who says it took about six weeks to bring all the Jewel stores live in Chicago, reports that Pay By Touch is in talks with Albertsons about further installations, but “no decision has been made” yet.

Meanwhile, Albertsons is being acquired by Eden Prairie, Minn.-based Supervalu, which with this deal is the owner of 15 grocery banners. Supervalu in January sold the Chicago-area Cub Foods stores to an investment group. According to Riordan, Albertsons and Pay By Touch originally planned to install the system in the standalone Osco pharmacies in the Chicago area as well, but had to pull back on that plan after CVS Corp. agreed to buy all standalone Osco outlets at the time of the Supervalu deal with Albertsons.

Up to now, Pay By Touch’s installations have covered too few stores in a market area to permit marketwide advertising to users. The company currently processes fingerprint scans for 2,000 merchant outlets around the country, including 1,600 that came to the company as a result of its recent acquisition of competitor BioPay LLC. Of these locations, about 70% are using the service to authenticate customers who are cashing payroll checks. These stores are not networked by Pay By Touch except with respect to the maintenance of a negative file. The remaining outlets are using it in-lane to authenticate customers who are paying for merchandise. These stores are networked so that a Pay By Touch user can make payments at any of the locations.

The authentication can secure credit and signature-debit transactions, but many merchants have opted to use it to authenticate customers for electronic checks on the automated clearing house. E-check transactions carry far lower fees to merchants than card payments, particularly given that acquirers apply card-not-present rates to biometrically secured transactions on card accounts unless a card is swiped. With Pay By Touch’s system, fingerprint scans replace cards, checks, or other payment tokens. The system matches fingerprint scans at the point of sale to mathematically derived templates obtained when customers enroll, then links transactions to payment accounts designated by customers.

Digital Transaction News

TV and Radio Advertising Campaign Slated to Begin April 5th

Electronic point-of-sale transactions secured by biometric scans may get a boost now that Pay By Touch Inc. has switched on processing service in 204 Jewel-Osco stores in the Chicago area.

Electronic point-of-sale transactions secured by biometric scans may get a boost now that Pay By Touch Inc. has switched on processing service in 204 Jewel-Osco stores in the Chicago area.The San Francisco company’s latest implementation represents its most concentrated installation in a metropolitan area so far. With many Jewel customers often shopping at more than one store in the chain, Pay By Touch hopes to get a lift in transaction volume. “This is the first time we’re going to see the network effect in action,” says Shannon Riordan, director of marketing for the company, whose technology allows merchants to authenticate customers via fingerprint scans. “We think that will be a driver of usage [in the Chicago area].”

In addition to the Jewel stores, Pay By Touch has been processing transactions for 35 Cub Foods stores in the Chicago metropolitan area for the past four months. These stores were until recently owned by Supervalu Inc.

TV and Radio Advertising Campaign

The market concentration also allows Pay By Touch to conduct marketwide consumer advertising for the service for the first time. Riordan says beginning in early April, advertising for the service will appear on radio and TV as well as in newspaper circulars placed by Jewel. “The time [for biometric payments] is now,” says Riordan. “It’s not a thing of the future any more.”

The Jewel installation follows a test by parent company Albertsons Inc. in four Portland, Ore., stores, which started in January 2005. Riordan, who says it took about six weeks to bring all the Jewel stores live in Chicago, reports that Pay By Touch is in talks with Albertsons about further installations, but “no decision has been made” yet.

Meanwhile, Albertsons is being acquired by Eden Prairie, Minn.-based Supervalu, which with this deal is the owner of 15 grocery banners. Supervalu in January sold the Chicago-area Cub Foods stores to an investment group. According to Riordan, Albertsons and Pay By Touch originally planned to install the system in the standalone Osco pharmacies in the Chicago area as well, but had to pull back on that plan after CVS Corp. agreed to buy all standalone Osco outlets at the time of the Supervalu deal with Albertsons.

Up to now, Pay By Touch’s installations have covered too few stores in a market area to permit marketwide advertising to users. The company currently processes fingerprint scans for 2,000 merchant outlets around the country, including 1,600 that came to the company as a result of its recent acquisition of competitor BioPay LLC. Of these locations, about 70% are using the service to authenticate customers who are cashing payroll checks. These stores are not networked by Pay By Touch except with respect to the maintenance of a negative file. The remaining outlets are using it in-lane to authenticate customers who are paying for merchandise. These stores are networked so that a Pay By Touch user can make payments at any of the locations.

The authentication can secure credit and signature-debit transactions, but many merchants have opted to use it to authenticate customers for electronic checks on the automated clearing house. E-check transactions carry far lower fees to merchants than card payments, particularly given that acquirers apply card-not-present rates to biometrically secured transactions on card accounts unless a card is swiped. With Pay By Touch’s system, fingerprint scans replace cards, checks, or other payment tokens. The system matches fingerprint scans at the point of sale to mathematically derived templates obtained when customers enroll, then links transactions to payment accounts designated by customers.

Digital Transaction News

Tuesday, March 21, 2006

Albertsons Introduces Pay By Touch

Introduces Pay By Touch Payment Systems to All of Its Jewel-Osco Stores in Midwest

BOISE, Idaho, March 21 /PRNewswire-FirstCall/ -- Albertson's, Inc. announced today that it is implementing Pay By Touch biometric payment systems in its Jewel-Osco stores throughout the Midwest. The rollout, which began in the Chicago area early this year and is expected to be completed in all 204 Jewel-Osco stores this month, follows a successful year-long test of the technology at Albertsons stores in the Portland, Oregon area. In the pilot program, a significant number of customers utilized the Pay By Touch option.

BOISE, Idaho, March 21 /PRNewswire-FirstCall/ -- Albertson's, Inc. announced today that it is implementing Pay By Touch biometric payment systems in its Jewel-Osco stores throughout the Midwest. The rollout, which began in the Chicago area early this year and is expected to be completed in all 204 Jewel-Osco stores this month, follows a successful year-long test of the technology at Albertsons stores in the Portland, Oregon area. In the pilot program, a significant number of customers utilized the Pay By Touch option.

Albertsons customers who used the technology in the company's Portland-area pilot program reported that they were convinced it is a faster, easier, and more secure way to pay for their groceries. The Jewel-Osco launch of Pay By Touch represents the largest market-wide launch of any retailer that has adopted the leading-edge technology.

"At Albertsons we are committed to helping make our customers' lives easier," said Pam Powell, Albertsons senior vice president of customer service. "With this technology, customers can pay for their groceries with the touch of a finger without having to present cards, checks, or cash, reduce their risk of theft and move through the checkout lines more easily and significantly faster."

"Pay By Touch is changing the way we pay for things today -- and in the years to come," said John Rogers, founder, chairman, and CEO of Pay By Touch Solutions. "Paying by touch gives shoppers the ultimate freedom from cards, checks, or cash that can be lost or stolen."

The Pay By Touch system, which is a free service for Jewel-Osco customers, uses a simple finger scan to authorize an electronic transaction from a customer's existing checking account while automatically honoring the Jewel-Osco Preferred Card. A one-time enrollment in the highly secure program takes only a few minutes to complete at Jewel-Osco stores. Customers may choose to link both their checking accounts and their Jewel-Osco Preferred Card to the Pay By Touch system.

About Albertsons

Albertsons is one of the world's largest food and drug retailers. The company's divisions and subsidiaries operate approximately 2,500 stores in 37 states across the U.S. and employ approximately 240,000 associates. Its banners include Albertsons, Acme, Shaw's, Jewel-Osco, Sav-on Drugs, Osco Drug, and Star Market, as well as Super Saver and Bristol Farms, which are operated independently. For more information about Albertsons, please visit our website at http://www.albertsons.com/.

About Pay By Touch

Pay By Touch is the global leader of biometric authentication, personalized rewards, and payment solutions. The company's patented biometric products and services enable shoppers to conveniently and securely access personal accounts using a finger scan to identify themselves, make purchases, cash checks, and earn rewards. Pay By Touch also provides robust payment processing solutions for ACH, card-present and card-not-present debit and credit transactions. To date, Pay By Touch services over 154,000 retail clients, manages personalized rewards programs for more than 130 million opt-in consumers, and has more than 2.3 million shoppers using biometric authentication products and services at 2,000+ locations coast to coast.

Founded in 2002, Pay By Touch is a privately held company headquartered in San Francisco that employs more than 500 professionals and holds more than two-dozen U.S. issued patents. For additional company information, visit http://www.paybytouch.com.

BOISE, Idaho, March 21 /PRNewswire-FirstCall/ -- Albertson's, Inc. announced today that it is implementing Pay By Touch biometric payment systems in its Jewel-Osco stores throughout the Midwest. The rollout, which began in the Chicago area early this year and is expected to be completed in all 204 Jewel-Osco stores this month, follows a successful year-long test of the technology at Albertsons stores in the Portland, Oregon area. In the pilot program, a significant number of customers utilized the Pay By Touch option.

BOISE, Idaho, March 21 /PRNewswire-FirstCall/ -- Albertson's, Inc. announced today that it is implementing Pay By Touch biometric payment systems in its Jewel-Osco stores throughout the Midwest. The rollout, which began in the Chicago area early this year and is expected to be completed in all 204 Jewel-Osco stores this month, follows a successful year-long test of the technology at Albertsons stores in the Portland, Oregon area. In the pilot program, a significant number of customers utilized the Pay By Touch option.Albertsons customers who used the technology in the company's Portland-area pilot program reported that they were convinced it is a faster, easier, and more secure way to pay for their groceries. The Jewel-Osco launch of Pay By Touch represents the largest market-wide launch of any retailer that has adopted the leading-edge technology.

"At Albertsons we are committed to helping make our customers' lives easier," said Pam Powell, Albertsons senior vice president of customer service. "With this technology, customers can pay for their groceries with the touch of a finger without having to present cards, checks, or cash, reduce their risk of theft and move through the checkout lines more easily and significantly faster."

"Pay By Touch is changing the way we pay for things today -- and in the years to come," said John Rogers, founder, chairman, and CEO of Pay By Touch Solutions. "Paying by touch gives shoppers the ultimate freedom from cards, checks, or cash that can be lost or stolen."

The Pay By Touch system, which is a free service for Jewel-Osco customers, uses a simple finger scan to authorize an electronic transaction from a customer's existing checking account while automatically honoring the Jewel-Osco Preferred Card. A one-time enrollment in the highly secure program takes only a few minutes to complete at Jewel-Osco stores. Customers may choose to link both their checking accounts and their Jewel-Osco Preferred Card to the Pay By Touch system.

About Albertsons

Albertsons is one of the world's largest food and drug retailers. The company's divisions and subsidiaries operate approximately 2,500 stores in 37 states across the U.S. and employ approximately 240,000 associates. Its banners include Albertsons, Acme, Shaw's, Jewel-Osco, Sav-on Drugs, Osco Drug, and Star Market, as well as Super Saver and Bristol Farms, which are operated independently. For more information about Albertsons, please visit our website at http://www.albertsons.com/.

About Pay By Touch

Pay By Touch is the global leader of biometric authentication, personalized rewards, and payment solutions. The company's patented biometric products and services enable shoppers to conveniently and securely access personal accounts using a finger scan to identify themselves, make purchases, cash checks, and earn rewards. Pay By Touch also provides robust payment processing solutions for ACH, card-present and card-not-present debit and credit transactions. To date, Pay By Touch services over 154,000 retail clients, manages personalized rewards programs for more than 130 million opt-in consumers, and has more than 2.3 million shoppers using biometric authentication products and services at 2,000+ locations coast to coast.

Founded in 2002, Pay By Touch is a privately held company headquartered in San Francisco that employs more than 500 professionals and holds more than two-dozen U.S. issued patents. For additional company information, visit http://www.paybytouch.com.

Wednesday, March 15, 2006

Monday, March 13, 2006

Losses Could Top $1 Billion in PIN Debit Fraud

The widening damage from the unfolding debit card hacking incident is challenging the conventional wisdom that PIN-based debit cards are inherently more secure than credit cards, which rely on signatures—though it still doesn’t make a case for chip cards. That’s according to one expert whose latest estimates are that this latest breach has so far affected far more than half a million cards and could cost consumers or their banks more than $1 billion.

The widening damage from the unfolding debit card hacking incident is challenging the conventional wisdom that PIN-based debit cards are inherently more secure than credit cards, which rely on signatures—though it still doesn’t make a case for chip cards. That’s according to one expert whose latest estimates are that this latest breach has so far affected far more than half a million cards and could cost consumers or their banks more than $1 billion.Through the use of magnetic-stripe systems such as card-verification values and a host of back-office security improvements invisible to cardholders, the credit card industry has driven down the fraud rate to less than half what it was 15 years ago. Today, the bank credit card fraud rate is only 5 basis points of transaction volume, according to analyst Avivah Litan, research vice president at Stamford, Conn.-based Gartner Inc.

Litan notes that while the latest debit card security compromise probably would not have happened if the cards had been chip-equipped smart cards, that still doesn’t create a business case for an expensive retrofit of the U.S. payment system for smart cards. Such an upgrade would cost billions because card issuers, merchants, and processors have so much invested in mag-stripe technology. “I think the solution is back-end fraud detection,” says Litan.

The recent debit card breach, which Litan estimates has compromised 600,000 cards and has forced at least 20 banks to reissue cards, shows also that PIN-based security is far more vulnerable than generally supposed. Indeed, Litan calls this the worst debit card compromise ever. She estimates direct consumer losses conservatively will be at least $100 million and could go as high as $1 billion or more, based on losses in previous incidents that ranged between $1,000 and $2,000 per account. “In terms of consumer impact, it’s definitely been the worst,” she says, adding that federal investigators are only about halfway through their probe.

Though details are far from complete, Litan and others who have talked to bankers and other informed sources believe computer hackers probably obtained stored card numbers and encrypted data, or so-called PIN blocks, linked to the personal identification numbers of debit cards used for purchases. They also apparently obtained the electronic “keys” that would allow them to de-encrypt the PIN blocks, and then connected the de-encrypted data with the correct card numbers. Then they were free to make bogus cards and withdraw cash at ATMs, which they did in several countries, until the issuers caught on and blocked the accounts.

Though details are far from complete, Litan and others who have talked to bankers and other informed sources believe computer hackers probably obtained stored card numbers and encrypted data, or so-called PIN blocks, linked to the personal identification numbers of debit cards used for purchases. They also apparently obtained the electronic “keys” that would allow them to de-encrypt the PIN blocks, and then connected the de-encrypted data with the correct card numbers. Then they were free to make bogus cards and withdraw cash at ATMs, which they did in several countries, until the issuers caught on and blocked the accounts.A California outlet of Itasca, Ill.-based office-products retailer OfficeMax Inc. has been named in various press accounts as a possible source of the breach, but OfficeMax has consistently denied having knowledge of a compromise, and Litan believes more than one retailer probably is involved.

While they don’t have inside knowledge of the investigation, Bill Pittman, president and founder of Redmond, Wash.-based payment software firm TPI Software LLC and Andrew Chau, TPI’s chief technical officer, say it is possible that software dubbed “middleware” may have made the breach possible. Middleware is a piece of software containing a master key that can de-encrypt PIN blocks, according to Chau. Normally such master keys are injected into point-of-sale PIN pads by transaction processors.

But merchants, particularly if they’re going to change processors, sometimes use middleware to store the keys themselves at their corporate headquarters. That saves them the hassle of making changes at individual terminals when changing over to a new processor.

Litan also says that while they’re not supposed to store card numbers and encrypted PIN data, retailers often do. That practice arises not from a deliberate flouting of the rules, but from the longstanding practices of computer programmers, who by nature store all manner of data.

“People store it just because they can,” she says.

Though much about the latest breach is unknown, the apparent theft of de-encryption keys shows to payment experts that the hackers may have had help from insiders, or at the very least were extremely knowledgeable outsiders. “I don’t think this was pure luck. This was a sophisticated operation,” says Pittman.

From Digital Transaction News

PIN scandal "worst hack ever"

PIN scandal "worst hack ever"; Citibank only the start

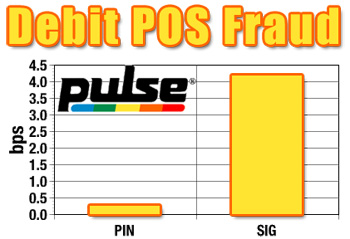

PIN scandal "worst hack ever"; Citibank only the start The article suggests that consumers "never" enter their PIN at the point of sale. If consumers adopt this behavior, then merchants will be foreced to pay the higher "signature debit" interchange rates on PIN debit transactions. Prior to this hack, PIN Debit Fraud at the POS was 16 times lower than signature debit. Visa announced it's Interchange rate would remain virtually unchanged from last year, but look for PIN debit rates to go up next year.

More importantly this creates a potential problem with the U.K.'s Chip and PIN program. Prior to this hack, some media outlets were suggesting that Pay by Touch may replace Chip and PIN. The timing of PBT's launch into Europe is also interesting because it coincides with a report by Unisys that 73% of Brits chose biometrics as the preferred technology in the fight against fraud.

More importantly this creates a potential problem with the U.K.'s Chip and PIN program. Prior to this hack, some media outlets were suggesting that Pay by Touch may replace Chip and PIN. The timing of PBT's launch into Europe is also interesting because it coincides with a report by Unisys that 73% of Brits chose biometrics as the preferred technology in the fight against fraud.{kind=link}

This is a developing story that will have a huge impact on the payments industry. If PIN's cannot be trusted at the point of sale, then what is the alternative? The writings on the wall.

http://www.abcmoney.co.uk/news/0920062125.htm

Sunday, March 12, 2006

Archive of PBT Posts

Previous PBT Posts

PINs No Obstacle for Debit Card Thieves

UK Survey - 73% Place Confidence in Biometrics

More European Retailers Looking at PBT

Superdividend for Pay by Touch

Pay by Touch Hits the UK

The Biometrics Are Coming...

Special News Feature

Jewel-Osco : Pay By Touch

High Touch Selling

Pay by Touch In-diapolis

Pay by Touch Introduces ATM Direct

Phishing Out...Keylogging In

Boston Globe Article

PBT Names Global VP of Biometrics

PBT in 100 Chicagoland Jewel Osco's

Video - Tech Closeup on Pay by Touch

Pay by Touch Launches in Colorado

John Morris to Present at Payments 2006

CardSystems Solutions Settles with FTC

M&A's - Landmark Year in Payments Industry

Bill Townsend Joins Pay by Touch

PBT Online at eTail 2006 and NACHA

Pay by Touch and BioPay FAQ

Health Care Firm to Sign with PBT

Pay by Touch Online Video Presentation

Consumer Closeup - Pay by Touch

PBT Expands into Financial Services

Pay by Touch Wins 3rd Award in 30 days

A Closer Look at PBT Loyalty Program

A Closer Look at PBT Online

Aite Group Report on Biometrics

A Closer Look at PBT's ATM Direct

60 Days of Breathless Activity

Walmart Going with Pay by Touch?

No One Knows How You Are Paying

On the Ball

Potential Future of Online Purchases

PBT Health Care Solutions Open for Biz

Pay by Touch going Global with NCR

Big Year Ahead for Pay by Touch

An EFT Network First...Biometric PIN Debit

Pay by Touch to Test PIN Debit on Web

Pay by Touch Brings Biometrics Home

Pay by Touch Wins INNY at DEMO 2006

Overcoming the Barrier to Adoption

Tech TV: Close Up with Pay by Touch

Pay by Touch Online

Pharming without Harming

Porter Novelli brings PBT to DEMO 2006

Quizno's Testing PBT

Star is Born

Jewel Osco implementing PBT

Cash Wise now "Biometrics" Wise

Capturing Resources

Pay by Touch Raises $190 million in three months

Customers Can't Wait to Sign Up

Report: Walmart, Costco looking at Pay by Touch

Motley Fool Names PBT Budding Rule Breaker

31 Patents with 70 Pending

Pay by Touch Wins Prestigious IBM Beacon Award

Contactless and Clueless

Biometric Payments Safest by Far

Don't Pay by Check...Pay by Touch!

Who's "Moe" Paranoid Now?

Thursday, March 9, 2006

PINs No Obstacle for Debit Card Thieves

PINs no obstacle for debit card thieves

This is an interesting development given the timing coincides with the launch of Pay by Touch in the U.K. The U.K. has just completed the implementation of their Chip and PIN technology and it has cut down significantly on fraud. With PIN's being compromised, fraud reduction may be short-lived.

This is an interesting development given the timing coincides with the launch of Pay by Touch in the U.K. The U.K. has just completed the implementation of their Chip and PIN technology and it has cut down significantly on fraud. With PIN's being compromised, fraud reduction may be short-lived.

The Mirror and ABC Money are reporting that PBT could dislodge Chip and PIN, however, because the Brits have invested $1.1 Billion in the nationwide implementation, I don't think that will happen.

This is an interesting development given the timing coincides with the launch of Pay by Touch in the U.K. The U.K. has just completed the implementation of their Chip and PIN technology and it has cut down significantly on fraud. With PIN's being compromised, fraud reduction may be short-lived.

This is an interesting development given the timing coincides with the launch of Pay by Touch in the U.K. The U.K. has just completed the implementation of their Chip and PIN technology and it has cut down significantly on fraud. With PIN's being compromised, fraud reduction may be short-lived. The Mirror and ABC Money are reporting that PBT could dislodge Chip and PIN, however, because the Brits have invested $1.1 Billion in the nationwide implementation, I don't think that will happen.

Here are the links to the articles.

Fingerprint system may dislodge chip-and-pin technology ABCmoney.co.uk, UK - Mar 9, 2006... Instead of keying in pin numbers, customers using the pay-by-touch have to get their fingerprints scanned by the scanners at the store checkout, which will ...

FINGERSCAN SYSTEM COULD MEAN END TO PAYING WITH CHIP-AND-PIN ...Mirror.co.uk, UK - Mar 8, 2006... "They are embracing Pay By Touch because it helps them get through the checkout faster without having to hunt for cards, cheques, wallets or purses.". ...

Wednesday, March 8, 2006

UK Survey - 73% Place Confidence in Biometrics

Unisys has announced survey results from the UK finding that UK consumers place most confidence in biometric technologies, such as fingerprint and eye retina recognition, to help combat identity theft.

The independent survey, commissioned by Unisys, surveyed 1,000 UK households to investigate the incidence of and attitudes towards financial fraud and solutions. The survey revealed that 2 in 3 consumers believe that banks should be turning to biometric technology in order to combat identity theft - a widespread problem which now affects 1 in 4 British adults according to Home Office statistics.

Despite token security being presented as an online authentication standard by some industry bodies, 92% of respondents were unfamiliar with the term and unaware of its use as a security measure. Once explained, only 42% of consumers believed that banks should adopt token security to help combat identity theft.

In comparison, the majority of respondents (73%) stated that biometric technology would assist banks in the fight against fraud and 48% placed confidence in smart cards.

Nigel Moden, Retail Banking Partner at Unisys explains: "Despite some historical resistance around biometric technology, the survey demonstrated a high level of support for this security method - with 73% of consumers placing confidence in biometrics ahead of token security rings and smart cards in the fight against fraud.

Whilst a thorough assessment of the prevention technologies available is critical when determining a strategy to combat fraudsters, banks must not overlook the attitudes and preferences of their customers in the process. Consumers are only going to use technology they are comfortable with and understand."

In addition, biometric technology now costs LESS to implement than Chip and PIN. Combine that with historical data derived from Pay by Touch implementations across the United States, and European retailers will have empirical evidence that biometrics increase average purchases, reduce identity theft and cost less than traditional payment methods such as cheques, credit and debit cards.

In addition, biometric technology now costs LESS to implement than Chip and PIN. Combine that with historical data derived from Pay by Touch implementations across the United States, and European retailers will have empirical evidence that biometrics increase average purchases, reduce identity theft and cost less than traditional payment methods such as cheques, credit and debit cards.The implementation by Midland Co-Operative of PBT (they already have data from trial runs and this is why they expect to roll this out to all 350 stores) will provide important data to other European Retailers (PBT is in negotiations with some large European retailers) The resulting data will be difficult to ignore when choosing whether or not to adopt this payment technology.

More European Retailers Looking at PBT

Co-op supermarkets introduce Pay by Touch Wed Mar 8, 2006 01:38 PM GMT

By David Burrows

LONDON (Reuters) - Just when consumers have got their heads around chip and pin, one supermarket has introduced payment verification by fingerprint. Three Co-op stores in the Oxford area are offering the service, which is already used in the United States but which is new to Europe.

Rather than signing for payment or keying in a pin number, customers using "pay-by-touch" need only set up an account at the store or online at home. There is no need to carry a card or cash, as the unique fingerprint is scanned at the store checkout and is immediately identified with a bank account which is then debited.

Simple perhaps, but civil liberties groups are wary of the scheme and predict possible problems in persuading shoppers to sign up without knowing who exactly would have access to their details.

Co-op, which is not charging customers to sign up, aims to introduce pay-by-touch to all its stores over time, a spokeswoman said.

The main selling point with biometrics is that only the individual in question can verify a payment or access an account, if it is used for online banking.

The US company that supplied Co-op stores with the scanners, Pay By Touch, says costs to retailers are not prohibitive. It is currently in negotiation with other big retail groups in Britain and Europe.

CHEAPER EQUIPMENT

Shannon Riordon, marketing director at Pay By Touch, told Reuters: "Scanners now cost just 40 pounds a unit, unlike a few years ago when they cost thousands.

"Now they are cheaper to install than chip and pin and most UK retailers will be watching to see how successful the Co-op scheme proves, and then we would expect many to follow suit."

Fingerprint technology will not be limited to over-the-counter sales. In time, consumers should be able to use fingerprint scanners at home and buy direct from online retail Web sites.

After investing so much in chip and pin technology, it remains to be seen how quickly major UK retailers will embrace biometrics.

While the system itself might prove cheaper to run, it relies on people signing up for the scheme and there will inevitably be issues relating to personal privacy as there have been with ID cards.

A spokeswoman for civil liberties group Liberty said: "I think it is a case of buyer beware. "Consumers need to know how the information is going to be used and who has access before they sign up. Undoubtedly the police will have access on request. (this is an incorrect statement as there is nothing to request...they're not fingerprints, but datapoints and the police could do nothing with them)

Regulation needs to be in place to ensure retailers adhere to data protection principles."

She added: "We do take on board the anti-fraud issue but would argue that all systems such as this are prone to human error."

© Reuters 2006. All Rights Reserved.

Superdividend for Pay by Touch

Pay by Touch will automatically award points and work with the Midland Cooperative's superdividend loyalty program.

The fourth largest co-operative society in the UK launched on 24 September. The Midcounties Co-operative brings together two former independant co-operative societies: Oxford, Swindon & Gloucester Co-operative and West Midlands Co-operative.

Bob Burlton, chief executive for The Midcounties Co-operative said, "This is a very exciting time for everyone. We are convinced that the combined Society will be more profitable and hence stronger then if we remained apart".

The Midcounties Co-operative runs 350 retail stores and a range of other businesses including retail, pharmacies, motor sales, childcare nurseries, care homes, funeral homes and more. 180,000 people are members of The Midcounties Co-operative and it employes 7,000 colleagues.

The Midcounties Co-operative runs 350 retail stores and a range of other businesses including retail, pharmacies, motor sales, childcare nurseries, care homes, funeral homes and more. 180,000 people are members of The Midcounties Co-operative and it employes 7,000 colleagues.The Society is the largest regional independent retailer in this area with an annual turnover of around £342 million, 125,000 members and over 4,000 employees.

The Society covers a geographical area which spans five counties, including most of Oxfordshire and Gloucestershire and the area around Swindon in Wiltshire. The Society is made up of six trading groups:

.

Pay by Touch Hits the UK

First European launch of a biometric payment system.

The Midcounties Co-operative goes live with its fingerscan payment system on March 8 starting in Oxford with its Headington store and following next week with its outlets in Carterton and

The Midcounties Co-operative goes live with its fingerscan payment system on March 8 starting in Oxford with its Headington store and following next week with its outlets in Carterton and  Summertown, also in Oxford.

Summertown, also in Oxford.

While researching different payment options, the Co-op – formed last year by the merger of Oxford, Swindon and Gloucester and the West Midlands co-ops – found the US based Pay by Touch company. They started a series of tests and pilots examined the data and the result is this week’s European launch of the system.

The Midcounties Co-op has gained a formidable reputation for its use of innovative technology and – as the OS&G – was one of the first in the country to introduce self-checkout systems four years ago.

The Pay by Touch system is gaining in popularity in the US although this is the first implementation in Europe. Customers register their fingerprint linked to specific payment cards and then simply pay by touching a fingerprint scanner in the store.

The database of prints is stored in the US by the IT vendor and in pre-launch trials it has taken three seconds for test prints to be approved.

“That is quicker that chip and PIN,” says Bill Laird, chief operating officer, trading, at Midcounties Co-op.

The Co-op started looking at fingerprint ID more than two years ago as a means of checking on shopper’s ages for alcohol purchases at its self-checkout units. “In Oxford we have a lot of students who often look younger than they are,” says Laird, “so we thought of fingerprint ID as a quick and efficient means of confirming their ages for self-checkout as otherwise supervisors had constantly to intervene and that slowed down the process and reduced the benefit.”

In the US retailers such as Thriftway in Seattle, have found wide acceptance for fingerprint payments. “We encourage shoppers to make their debit card the first choice card payment when they register,” says Paul Kapioski, president and owner of CAP Food Services which runs Thriftway.

“This has helped drive payments away from credit cards which are more expensive for us to accept.”As a result debit card transactions at the store have increased from 38% to 64% in the past two years. Since card transactions payments are 72c for credit and 32c for debit payments this clearly represents significant payback for the scheme.

According to Kapioski in the first 12 weeks of implementation some 25,000 customer enrolled for Pay by Touch and chargebacks have declined from four to five a month to just two in the past year. “It is a real deterrent to fraudsters,” he says, “and has also increased throughput at our checkouts.” The system has proved especially popular with the elderly who now feel more secure when they shop as they have no need to bring cash or cards to the store so are less fearful of potential muggers.

At Oxford, Bill Laird is confident of similar results: “Initial reaction from test shoppers is very positive,” he says.

The Midcounties Co-operative goes live with its fingerscan payment system on March 8 starting in Oxford with its Headington store and following next week with its outlets in Carterton and  Summertown, also in Oxford.

Summertown, also in Oxford.While researching different payment options, the Co-op – formed last year by the merger of Oxford, Swindon and Gloucester and the West Midlands co-ops – found the US based Pay by Touch company. They started a series of tests and pilots examined the data and the result is this week’s European launch of the system.

The Midcounties Co-op has gained a formidable reputation for its use of innovative technology and – as the OS&G – was one of the first in the country to introduce self-checkout systems four years ago.

The Pay by Touch system is gaining in popularity in the US although this is the first implementation in Europe. Customers register their fingerprint linked to specific payment cards and then simply pay by touching a fingerprint scanner in the store.

The database of prints is stored in the US by the IT vendor and in pre-launch trials it has taken three seconds for test prints to be approved.

“That is quicker that chip and PIN,” says Bill Laird, chief operating officer, trading, at Midcounties Co-op.

The Co-op started looking at fingerprint ID more than two years ago as a means of checking on shopper’s ages for alcohol purchases at its self-checkout units. “In Oxford we have a lot of students who often look younger than they are,” says Laird, “so we thought of fingerprint ID as a quick and efficient means of confirming their ages for self-checkout as otherwise supervisors had constantly to intervene and that slowed down the process and reduced the benefit.”

In the US retailers such as Thriftway in Seattle, have found wide acceptance for fingerprint payments. “We encourage shoppers to make their debit card the first choice card payment when they register,” says Paul Kapioski, president and owner of CAP Food Services which runs Thriftway.

“This has helped drive payments away from credit cards which are more expensive for us to accept.”As a result debit card transactions at the store have increased from 38% to 64% in the past two years. Since card transactions payments are 72c for credit and 32c for debit payments this clearly represents significant payback for the scheme.

According to Kapioski in the first 12 weeks of implementation some 25,000 customer enrolled for Pay by Touch and chargebacks have declined from four to five a month to just two in the past year. “It is a real deterrent to fraudsters,” he says, “and has also increased throughput at our checkouts.” The system has proved especially popular with the elderly who now feel more secure when they shop as they have no need to bring cash or cards to the store so are less fearful of potential muggers.

At Oxford, Bill Laird is confident of similar results: “Initial reaction from test shoppers is very positive,” he says.

The Biometrics Are Coming...

The English love nothing better than a nice long queue, but supermarket lines could soon be under threat – a new speedy finger scan payment system has just been launched in the UK.

The English love nothing better than a nice long queue, but supermarket lines could soon be under threat – a new speedy finger scan payment system has just been launched in the UK.Developed by biometric giant Pay By Touch, the service will initially be available in three Midcounties Co-op supermarkets in Oxford and will spread to other stores if successful. The sign-up process sounds straightforward enough: you just apply for the free service in-store or on the net, and your account is then activated when you visit a participating store. After that, you get automatically rewarded for your buys with Co-op dividend points. According to Pay By Touch, the system has been very successful in the US where 2.3 million (and growing) shoppers already use it.

Paying for goods using Pay By Touch takes around ten seconds. The system is available in the UK at three Mid-Counties Co-op shops in Oxford, with plans to roll out in Swindon and Gloucester later on. The initial sign up process can be completed either at home on the Internet or in store. The service is then activated when the consumer visits the supermarket.

Bill Laird, COO, retail, Midcounties Co-op, says: "Our customers are embracing Pay By Touch because it helps them get through the checkout faster without having to hunt for cards, cheques, wallets or purses."

UK shoppers can now pay for goods without cash, cards or cheques, using the new Pay By Touch system. Chip ‘n’ Pin terminals have reduced fraud by 24% this year, but, nevertheless have come under fire for being susceptible to the roaming eyes of thieving "scallywags". Pay By Touch is adamant that the initial response from its trial users has been ‘very encouraging’.

People wishing to check out the new system can find the stores at Co-ops on:

152 London Road, Headington, Oxford;

Blackbourton Road, Carterton, Oxfordshire; and at

228-240 Banbury Road, Summertown, Oxford.

For Coverage Visit the Links Below:

Shoppers pay by fingerprint Edinburgh Evening News, UK

Co-op stores in the Oxford area are offering the service, which is said to be the first of its kind in Europe. It means shoppers ...

Don't forget your finger Find.co.uk, UK

Soon, you won't need to remember your wallet or even your pesky chip and pin digits when you go to the shops, thanks to a new system set to ...

Fingerprints 'point' to anti-ID theft safeguard 24dash.com, UK

Identity fraud remains the fastest rising crime in the UK but fingerprints could point the way towards prevention. The Co-Operative ...

Supermarket launches fingerprint payments InTheNews.co.uk, UK

A leading UK supermarket chain has launched a trial scheme enabling customers to pay for their purchases by touching a finger on a scanner. ...

UK's Midcounties Co-op live with Pay By Touch biometric payments ...Finextra, UK -

California-based Pay By Touch says its biometric authentication technology has been rolled out at Midcounties Co-operative supermarkets in the UK. ...

Pay By Touch goes live MyFinances.co.uk, UK

UK shoppers can now pay for goods without cash, cards or cheques, using the new Pay By Touch system. Under the new system, fingerprint ...

Co-op goes live with fingerprint payments Retail Bulletin, UK

The Midcounties Co-operative goes live with its fingerprint payment system on March 8 starting in Oxford with its Headington store and following next week with ...

Pay By Touch hits the UK Stuff Magazine, UK

The English love nothing better than a nice long queue, but supermarket lines could soon be under threat – a new speedy finger scan payment system has just ...

Friday, March 3, 2006

Special News Feature

Special News Feature in Transaction World Magazine March 2006

Pay By Touch, San Francisco, Calif., was on the acquisition trail at the end of 2005 and is starting to emerge as a small, but significant player in the acquiring business, according to Les Riedl, President of Speer & Associates, Atlanta, Ga.

Pay By Touch’s specialty is biometrics, but with the recent acquisitions and others that could be made, Riedl expects the biometrics portion of the business to become an ever-smaller portion of the total enterprise. Riedl sees that as good for Pay By Touch’s long-term prospects because biometrics today has a small niche market and growth prospects are iffy. Though the pilot merchants using Pay By Touch’s biometric solutions like it, consumers as a whole still aren’t all that sold on the technology. This may be due to a heightened sense of privacy concerns after all of the publicity surrounding identity theft.

A quick look at Pay By Touch’s recent acquisitions:

The assets of CardSystems Solutions, Inc., a payment processing provider. Under the terms of the deal, Pay By Touch assumed responsibility for all CardSystems Solutions, Inc. assets and for payment relationships with reportedly 120,000 small and medium-sized merchants. The deal was completed primarily for stock and some cash. CardSystems provides integrated payment solutions to associations, financial institutions and independent sales organizations and retail merchants. Through these payment solutions, CardSystems processes more than $18 billion in Visa, Mastercard, American Express, Discover, online debit and EBT transactions annually. www.paybytouchpaymentsolutions.com

7th Street Software, Inc. and Convena, LLC, two loyalty technology providers that Pay By Touch officials expect to significantly bolster the company’s loyalty offerings. 7th Street Software, Inc. is the developer of LoyaltySuite, a patent-pending technology that helps retailers automatically give shoppers personalized offers on the products they purchase most. The Convena, LLC assets add another layer to Pay By Touch’s loyalty offerings.

7th Street Software, Inc. and Convena, LLC, two loyalty technology providers that Pay By Touch officials expect to significantly bolster the company’s loyalty offerings. 7th Street Software, Inc. is the developer of LoyaltySuite, a patent-pending technology that helps retailers automatically give shoppers personalized offers on the products they purchase most. The Convena, LLC assets add another layer to Pay By Touch’s loyalty offerings. Capture Resource, a supplier of integrated reward programs and business process outsourcing solutions, further enhancing the company’s loyalty offerings. This acquisition enables Pay By Touch to offer customers interactive gift and reward programs, customized reporting, design, production, and Web access services. In addition, the company will offer retailers advanced information capture technology and database management. Pay By Touch assumes responsibility for all of Capture Resource, Inc. assets and will manage the company’s 120 million-plus consumer loyalty enrollment profiles, including more than 12,000 supermarkets and retail institutions. www.captureresource.com

Capture Resource, a supplier of integrated reward programs and business process outsourcing solutions, further enhancing the company’s loyalty offerings. This acquisition enables Pay By Touch to offer customers interactive gift and reward programs, customized reporting, design, production, and Web access services. In addition, the company will offer retailers advanced information capture technology and database management. Pay By Touch assumes responsibility for all of Capture Resource, Inc. assets and will manage the company’s 120 million-plus consumer loyalty enrollment profiles, including more than 12,000 supermarkets and retail institutions. www.captureresource.comBioPay is a biometric services provider with two million enrolled consumers, 1,600 retail implementations, and more than $7 billion in transactions processed. BioPay specialized in biometrically authenticated check cashing, with more than 2 million consumers in retailers across 42 states. The deal was expected to close in the first quarter of 2006. www.biopay.com

ATM Direct

ATM DirectATM Direct has a patent-pending software only PIN Debit solution for Internet transactions. They will incorporate the technology into the recently introduced Pay by Touch Online platform. www.atmdirect.com

The company continues to expand its merchant base as well. In early January of this year, 10 more grocery stores in Minnesota and North Dakota added Pay By Touch payment capabilities, adding to the estimated 2 million consumers that were already using the firm’s biometric payment solution, according to the company. Yet the total market for biometric payments is still small, according to Riedl and Marc Abbey, Analyst for First Annapolis Consulting, Annapolis, Md. Beyond grocery stores, the biometric payments have yet to catch on in other industries. The Pay By Touch technology has worked in the grocery stores because they are payment-intensive businesses with low margins and low returns on sales – so owners are willing to experiment on new, low-cost types of payments, Abbey says. Other types of businesses haven’t been as willing to experiment with new types of payment technologies.

“It’s an intriguing company, they have a lot of momentum,” Abbey adds. “Ever since they acquired InterCept, they’ve been building out their capabilities. But there are significant questions if biometrics itself has a broad enough appeal in the marketplace.

They’re a lot further along than I thought they would be at this point.” The technology itself is far ahead of the business applications for it, Abbey adds. “The interest on the consumer end is the weak link. Only time will tell how successful they will be.” Part of the reason for the company’s success so far is the financial wherewithal of the firm’s owners Riedel says. “They have a ton of money behind it.”

Thursday, March 2, 2006

Jewel-Osco : Pay By Touch

Click the link below to see where you can use Pay by Touch

in Albertson's Jewel Osco Stores in the Greater Chicagoland Area.

High Touch Selling

Biometric technology takes center stage at NGA's Technology Symposium. MARCH 01, 2006

Single-store independent Green Hills, based in Syracuse, N.Y., is pioneering the use of biometric payment technology to create promotions that target shoppers individually. "

Single-store independent Green Hills, based in Syracuse, N.Y., is pioneering the use of biometric payment technology to create promotions that target shoppers individually. "

Grocers go to market using channels that aren't really effective," said v.p. Sterling Hawkins, who spoke last month at the National Grocers Association's Technology Symposium. "In 1965 Procter & Gamble only needed three 30-second TV spots in order to reach their audience. Today that number stands at 117. Trade promotions are decreasing in effectiveness, as are coupons, which are down to a 1.3 percent redemption rate."

He noted that less than 10 percent of Green Hills' customers were buying items that were on the front page of their ad fliers. What's more, less than 1 percent were buying products from the inside of the ad. "We also see that our loyal customers are receiving a disproportionate amount of our marketing spend," said Hawkins. "The convenient shoppers are receiving much more than they deserve, leaving what little is left over for the loyal shoppers. Added to this, we were seeing a huge amount of customer variance. The top 5 percent of our customers were generating 33 percent of our total sales, while the bottom 30 percent of our customers were generating less than 1 percent. Those best customers are also shopping more frequently: 127 times a year, spending more each time they visit, and staying with us over longer periods of time.

"To address this, Green Hills leveraged its biometric payment system, supplied by San Francisco-based Pay By Touch, to provide individual customers with relevant, timely, and differentiated offers to maximize their shopper lifetime value, delivered to the POS with the touch of a finger.

Here's how it works: Green Hills shoppers sign up for the loyalty program as they enroll with the biometric payment system. In addition to their payment options, such as credit and debit cards, they can add the loyalty program to their "electronic wallet.

Single-store independent Green Hills, based in Syracuse, N.Y., is pioneering the use of biometric payment technology to create promotions that target shoppers individually. "

Single-store independent Green Hills, based in Syracuse, N.Y., is pioneering the use of biometric payment technology to create promotions that target shoppers individually. "Grocers go to market using channels that aren't really effective," said v.p. Sterling Hawkins, who spoke last month at the National Grocers Association's Technology Symposium. "In 1965 Procter & Gamble only needed three 30-second TV spots in order to reach their audience. Today that number stands at 117. Trade promotions are decreasing in effectiveness, as are coupons, which are down to a 1.3 percent redemption rate."

He noted that less than 10 percent of Green Hills' customers were buying items that were on the front page of their ad fliers. What's more, less than 1 percent were buying products from the inside of the ad. "We also see that our loyal customers are receiving a disproportionate amount of our marketing spend," said Hawkins. "The convenient shoppers are receiving much more than they deserve, leaving what little is left over for the loyal shoppers. Added to this, we were seeing a huge amount of customer variance. The top 5 percent of our customers were generating 33 percent of our total sales, while the bottom 30 percent of our customers were generating less than 1 percent. Those best customers are also shopping more frequently: 127 times a year, spending more each time they visit, and staying with us over longer periods of time.

"To address this, Green Hills leveraged its biometric payment system, supplied by San Francisco-based Pay By Touch, to provide individual customers with relevant, timely, and differentiated offers to maximize their shopper lifetime value, delivered to the POS with the touch of a finger.

Here's how it works: Green Hills shoppers sign up for the loyalty program as they enroll with the biometric payment system. In addition to their payment options, such as credit and debit cards, they can add the loyalty program to their "electronic wallet.

{kind=link}

"Each week every customer household receives a set of personalized offers that's customized to it, and when the consumers shop, these offers are delivered to them at the POS when they scan their finger." There are no coupons, no cards," said Hawkins. "We also have a Web-based shopping utility where shoppers can log on and view and manage their shopping list, or print it out at a kiosk in the store using just their finger." Using the system, Green Hills is able to run multiple reward programs for any one individual, as well as different programs for different individuals. "I may be in the steak club, he may be in the soda club, but we're both in the Thanksgiving turkey promotion. This way customers are in control of when, where, and how they receive their marketing communications.

"Each week every customer household receives a set of personalized offers that's customized to it, and when the consumers shop, these offers are delivered to them at the POS when they scan their finger." There are no coupons, no cards," said Hawkins. "We also have a Web-based shopping utility where shoppers can log on and view and manage their shopping list, or print it out at a kiosk in the store using just their finger." Using the system, Green Hills is able to run multiple reward programs for any one individual, as well as different programs for different individuals. "I may be in the steak club, he may be in the soda club, but we're both in the Thanksgiving turkey promotion. This way customers are in control of when, where, and how they receive their marketing communications.As such, they can view them by the Pay By Touch system, via e-mail, or on a personalized Web page, and the infrastructure is built to support any digital device that gains critical mass, such as cell phones."Currently the system is up and running with Green Hills' 200 employees, and is set to go public in just a few weeks.

Missouri's first biometricsEnhanced security, cost savings, and shopper convenience drove St. Charles, Mo.-based Mid-Towne IGA's decision to install a biometric payment system in its store last November, according to v.p. of operations Scott Kohrs, who also spoke at NGA's Technology Symposium. The system, from BioPay (now owned by Pay By Touch), has already generated results: ( Pay By Touch Buys BioPay for $82 Million )

"Our average transaction size with someone paying using the BioPay system was nearly $40, while our typical transaction size is in the neighborhood of $20, so they're spending more with this technology," said Kohrs. "We haven't had any fraudulent payments since we started with this program in November. Plus it has generated lots of local and national attention, which brings people into the store. "The system also offers more security for shoppers enrolled in the system, noted Kohrs. "Customers, once they are enrolled, can literally shop without their purse or wallet," he said. "As a result you can't have your credit card numbers stolen.

{kind=link}

In the case of a regular personal check, not many people realize this, but it will pass through anywhere from eight to 12 people's hands before it's returned. So it may seem like a secure thing because consumers are used to it, but in reality there are many opportunities for people to take advantage of it.

"In addition to its loss prevention benefits, Kohrs found that biometric technology helps cut transaction costs as well. "Typically the national average for a credit card or debit card transaction is from 80 cents to as much as $1.80 or more per transaction," he noted. "In our case, we use a check-cashing service, so by the time everything is said and done, with bank charges included, a check is now in the range of $1 per transaction. With BioPay, a typical transaction under $100 costs 20 cents."

Because of this, last month Kohrs began phasing out the payments by paper check with a "check replacement" program, during which store associates will encourage these shoppers to switch their payments to the biometric system. Although Kohrs expects to lose some diehard check writers, he predicts they'll be back before long, once they realize how simple the biometric payment system is to use.

Paper checks are the only form of payment Kohrs wants to get rid of, he stressed. "We're not seeking to eliminate debit cards and credit cards—I think those will be around forever," he said. "For the most part, we're looking to get rid of the check-writing customer. We feel that's one of the biggest areas of fraud, and we end up chasing down a lot of $25 checks. [The new program] is one of the main ways you can save some money and some headaches." One side benefit the biometric payment system delivered was exposure.